| OCR Text |

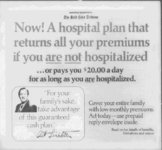

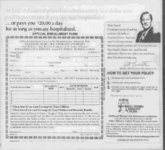

Show Imagine-- a hospital plan that protects you j but may end up costing you nothing. This is a hospital plan for people who get sick." If you're one of them, please keep reading. You're probably under 45. If not, you're what people call "the picture of health." Probably had nothing worse than a little cold or indigestion from overeating since you "can't remember when." You figure, who needs hospital insurance? Maybe you're right. But suppose you're wrong? After all, over 30 million people will go to the hospital this year. And you could be one of them. Why gamble with your health or your family's when right now it's so easy for you to "play it safe"? At last a hospital plan tailor-mad- e for healthy people. We call it the Guaranteed Cash Plan. It's different from other plans. We pay you cash benefits whether you stay healthy or go to the hospital. Here's the way the plan works. If you are hospitalized, you get $20.00 a day paid directly to you, to use as you see fit. If you don't go to the hospital you still collect from this plan. Yes, if you or a covered adult member of your family receives no benefits during 10 years of continuous coverage, the premiums you paid for yourself or for that family member are returned to you in full. Even if another adult family member collects benefits, you still may get a premium refund. And if you don't collect benefits for your children during that peri od, you will receive a full refund of their premiums, too! As you can see, this plan may cost you absolutely nothing. j We want you to try it for a month. Can you spare a quarter? Because that's all it costs to try the plan. This 254 premium will cover you and your entire family for a month. Then if you like the plan, you may ? continue at renewal rates as low as $4.55. If i you don't, you can cancel out. (We'll even j ' return your quarter.) How can you lose? r ? "But I already have hospitalization insurance." Fine. But even if you have a Blue Cross Hospitalization Plan, Blue Shield Medical 3 Plan, or any other health plan, keep it. But remember, plans like these may not pay all the bills. Many basic plans don't cover Many doctor bills. Transfusions. j; Ambu- - lance service. Orthopedic aids. Drugs. Medicines. nursing care. Many how much they'll limit set also a on plans than that Worse how and for long. pay none of these plans pays one cent toward Post-hospit- al household bills that never stop . . . ? even when you're in the hospital. The rent, tele- phone, electricity, food, kids' clothing, etc. You get the idea. Dear Friend: I wouldn't recommend anything I And I didn't honestly believe in. think National Home's $20.00-a-da- y plan is just about the best additional protection you can give your family especially with its wonderful money-bafeature It's a health plan that returns all the money a policyowner ck ! has paid in premiums. That's another reason I'm happy to give this plan endorsement. Since I am a stockholder and retained as a marketing consultant, I've made a point of getting to know some of the folks at National Home. I've seen the way they handle claims, too quickly and efficiently. Believe me, when you need them, they'll be there to help you. That's why I cannot imagine anybody passing up the chance to enroll in this health plan especially when you remember that you get paid whether you go to the hospital or stay well. How can you beat a hospital plan my wholehearted that guarantees you benefits if you and returns every are hospitalized dollar you paid if you stay well? So don't wait. Read this booklet carefully you'll be glad you did. Sincerely, j That's what the National Home Guaran- - i Art Linkletter teed Cash Plan is for: to help pay bills basic Member of lAie health plans may not pay! National Home Board of Directors, Life Assurance Company |